The European photovoltaic installation market is addressing challenges to grid connection, including complex permitting and lengthy wait times.

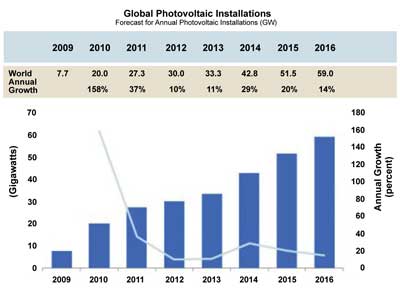

Solar power, now the third most important renewable energy source in terms of globally installed capacity after hydro and wind power, faced slowed growth in 2012. This was the year to survive for many photovoltaic (PV) players, as a global explosion of production capacity caught up with the industry. While growth of global PV installation was 35 percent from 2010 to 2011, it slowed to just 10 percent in 2012, according to IMS Research of Wellingborough, UK (Figure 1).1

Figure 1. Growth of global PV installations slowed to 10 percent in 2012 and is expected to remain sluggish in 2013; however, it should improve again once overstocked inventory is depleted. Courtesy of IMS Research, July 2012.

The PV installation market is subject to an uncertain and ever-changing political landscape. As generous incentives and feed-in tariff (FIT) schemes in several countries expired or were reduced in 2012, demand quickly receded. The result was a teetering tower of overstock everywhere in the supply chain and overhanging production capacity, just as companies were ramping up to meet the growth they were seeing.

These cuts to FITs and incentive schemes are the main issue currently affecting PV demand in Europe, according to Lauren Cook, market analyst at IMS. “The uncertainty caused by incentive cuts leads to peaks in demand as people rush to install before the incentives expire. This is followed by subsequent slowdowns in the market.”

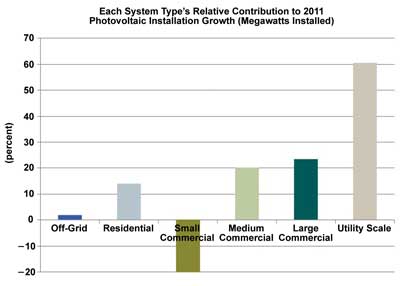

Among the four photovoltaic system types – ground-based, rooftop, building-integrated and off-grid systems – the current general trend in European installations is toward smaller rooftop installations, Cook said (Figure 2). This is another result of lowered tariffs and reduced incentives in Germany and Italy for larger systems. While utility-scale installations still accounted for the largest growth in 2011 (Figure 3), IMS Research predicts that utility-scale installations in Germany will decline by more than 60 percent in 2013 following the cuts to incentives for large systems.

Figure 2. The current reduction in incentives has led to an uptick in the percentage of smaller, rooftop installations in Europe, such as this one in Ingolstadt, Germany. Courtesy of QCells.

In 2012, the biggest European installations have been built in Germany (Figure 4). In the second and third financial quarters, several of these took advantage of the grace period after FIT cuts in April, Cook said, adding that “some large installations in Spain may be possible outside of incentive schemes in a few years’ time using power purchase agreements, but it will take some time for these projects to be realized.”

After the dust settled in 2011, the European Photovoltaic Industry Association (EPIA) listed Italy as the top market for grid-connected power in Europe; Italy quadrupled its capacity to 9.3 GW of newly connected systems due to the more advantageous FITs that occurred in 2010 (Figure 5). It was the first time that Germany was displaced as the top European country for grid-connected installations. Germany followed in second place in 2011 with 7.5 GW, helped by a mild winter and a late-year rush to take advantage of FITs in anticipation of reductions. Italy and Germany accounted for nearly 60 percent of the global grid connections in 2011.

Figure 3. In 2011, more than 60 percent of global PV installations were utility-scale, followed by large commercial installations. Small commercial installations experienced negative growth. Courtesy of IMS Research, November 2011.

In comparison, as of April 2012, new figures from IMS Research revealed that new global photovoltaic installations (not necessarily grid-connected) surpassed 13 GW in the first six months of 2012. In the second half of the year, almost 18 GW is expected to be added. By year’s end, Germany, China and the US will be the leading markets, in that order, and Italy will be in fourth place.2

Disconnect

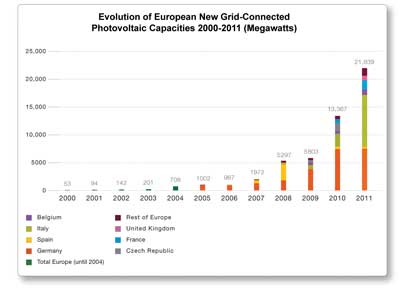

Part of the challenge to stable solar growth is the disconnect between installed, operating solar panels and those connected to the power grid. In Europe, approximately 21.9 GW of solar was connected to the grid in 2011, according to the EPIA’s report Global Market Outlook for Photovoltaics Until 2016, released in May 2012.3 In comparison, IMS Research estimates that 18.9 GW of solar was “installed.” Typically, a significant time lag exists between installing a solar panel and grid connection; in this case, however, the lower number from IMS reflects a large volume of systems installed toward the end of 2010 and connected at the beginning of 2011.

Figure 4. The majority of installations in Europe are on the massive utility scale, such as this one in Briest, Germany. Courtesy of QCells.

While many European countries have implemented favorable PV legislation and support policies, many barriers hamper the actual construction of PV projects. Grid connection of photovoltaic systems can take months and even years as a result of lengthy bureaucratic procedures and highly complex requirements, including notification, registration, licensing and an environmental impact assessment. Installers face unclear interpretation of rules and excessive costs in many markets. As such, an initiative of more than 10 national PV associations, including the German Solar Industry Association, BSW-Solar; EPIA; and many others began a two-and-a-half-year EU-funded initiative called PV LEGAL in July 2009 to identify and reduce legal and administrative barriers to PV installation in Europe.4

The first phase of the initiative involved creating an extensive database identifying bureaucratic barriers faced by project developers in selected countries. The database categorizes barriers by country and the relevant PV sector. For example, in Germany, where medium-size to large rooftop systems on industry and commercial buildings made up about 74 percent of the German PV market in 2010, the grid connection application is a frequent significant obstacle.5

For systems with more than 30 kilowatt-peak (kWp) power, the most favorable connection point is not defined by law as it is for systems up to 30 kWp. According to the database, “The grid operator has more leeway than with small systems to make the connection of the system more difficult. Experiences with the individual grid operators differ greatly. System operators have to expect long wait times and some inappropriate fees.”

Figure 5. The EPIA estimates that in 2011, Italy surpassed Germany in new grid-connected PV capacity. The growth in diverse markets across Europe will help stablize the effect of the reduction in incentives experienced in Germany and Italy. Courtesy of EPIA.

Near the end of the initiative, in February 2012, some countries had seen improvements. For example, France, Greece, Germany, the Netherlands and Portugal now have online registration systems, less stringent permitting requirements and one-stop-shop systems that help reduce the time required to register and install residential systems.6

But elsewhere in Europe, serious issues still remain. Developing a commercial rooftop system through overly burdensome bureaucracies in Spain, Bulgaria and the UK can take as long as 89 weeks.7 Complying with these regulations and grid connection processes represents almost half the development cost of a project.

The final PV LEGAL report issued a set of key recommendations for overcoming these barriers as identified in various countries. The most problematic administrative barriers to grid connection include complex and unclear permitting procedures, grid connection rules and technical standards in need of stream-lining, and grid capacity issues. The PV LEGAL project found that “despite some progress, many EU Member States must still remove obstacles to the deployment of renewable energy systems, especially solar PV.”8

“The program was very successful,” said Thomas Chrometzka, head of international affairs for BSW Solar. “We identified all the removable administrative barriers hampering the large-scale integration of photovoltaic power into electricity distribution systems, and will follow up this project with a new initiative, called PV GRID. The goal of the PV GRID project is to analyze the barriers and formulate regulatory and normative recommendations to facilitate grid integration.” The PV GRID project, which began ramping up in October 2012, will track additional countries in the database. The project will also broaden to include distribution system operators.

“We will start our communication activities regarding the project in November/December with the update of the PV LEGAL database,” Chrometzka said. “The recommendations on better grid integration will follow.”

Growth ahead

There is hope for the future of solar. “PV is no longer a niche product,” said Reinhold Buttgereit, EPIA’s secretary general. “It is an increasingly important source of electricity generation. This means we have to start thinking differently about it. Integrating PV seamlessly into the electricity grid will require some changes from grid operators, policymakers and from the PV industry itself. But the challenges are not insurmountable.”

In a newly released report, Solar Annual 2012: The Next Wave, PHOTON Consulting of Boston forecasts that the current PV downturn will be followed by a new wave of renewed PV demand. The “next wave” will be a period of tremendous, unprecedented growth with global installations reaching 46 GW by 2015, the report predicts. The trick of future survival for the plethora of solar companies out there today will be to anticipate conditions and take action now.

“Solar power’s transition to widespread rate parity – while turbulent – is the start of a new phase in the industry’s growth and global adoption,” said Chris Bolman, senior analyst at PHOTON Consulting. “The current turmoil and the ‘next wave’ will rationalize the industry’s supply-demand balance, bring needed solar electrification to new markets, and create new opportunities for entrepreneurs, innovators and forward-thinking energy companies.”

Whether the PV industry can become profitable on its own, reaching grid parity with legacy energy without the lure of government credits and FIT schemes to support it, depends on the efforts of, and careful planning by, legislators, industry leaders and PV players all along the market supply chain from silicon to grid connection.

References

1. Global Installation PV forecast through 2016, IMS Research: http://www.pvmarketresearch.com/free-resources/research-data.php

2. PV Demand Quarterly, IMS Research: http://www.pvmarketresearch.com/report/PV_Demand_Database_Quarterly_Q212

3. Global Market Outlook for Photovoltaics Until 2016, EPIA: http://templatelab.com/Global-Market-Outlook-2016/

4. PV LEGAL Key Recommendations: http://www.pvlegal.eu/en/results/key-recommendations.html

5. PV LEGAL Database: http://www.pvlegal.eu/nc/en/database.html

6. PV LEGAL Status Report: http://www.pvlegal.eu/fr/results/status-reports.html

7. Global Market Outline Through 2016, EPIA

8. PV LEGAL press release: http://www.pvlegal.eu/fr/press/press-releases.html