Jacques Cochard, Tematys and Carlos Lee, EPIC

A new report details opportunities for photonics in the life sciences and medicine.

Biophotonic technologies have received more and more attention in recent years, highly touted as more-effective, cost-saving methods with applications ranging from medicine to life sciences research and beyond. In the wake of the bubble bursts in the telecom and solar industries, cautious CEOs might wonder whether the hype surrounding biophotonics is leading up to the same thing – bubble and burst – and, if not, what the opportunities might be for components manufacturers in this booming market.

EPIC (European Photonics Industry Consortium) recently released a report outlining opportunities in the biophotonics value chain; the report was carried out by Tematys and Yole Développement in close collaboration.

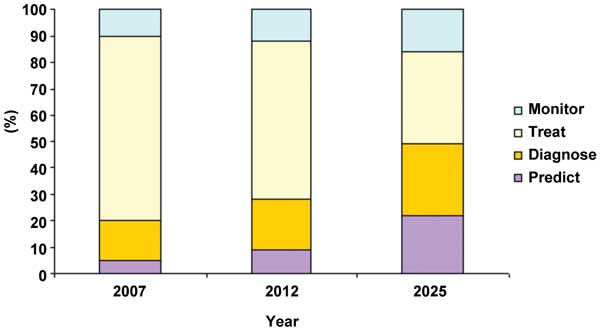

Diagnostic and monitoring applications are paving the way for new optical technologies. Over the past 20 years, countries within the Organisation for Economic Co-operation and Development (OECD) have faced increased growth of the pensioner population as well as recurrent epidemics, chronic diseases and economic issues linked to unsustainable, unbalanced health care systems. Today, health care is moving from a treatment-oriented system to a diagnostic-oriented one, as highlighted by the statistics in Figure 1, which show that the portion of global health care spending devoted to treatment (chemotherapy, drugs, etc.) will decrease from 70 percent to less than 40 percent in the next 15 years. The end goal of this evolution is regular monitoring of health and ongoing treatment efficiency evaluations – personalized medicine – which is promising but still far away.

Figure 1. Global health care spending (source: Frost & Sullivan, 2009). Courtesy of Tematys SARL.

Miniaturization is a major trend in every industry sector, and health care is no exception. The agriculture industry faces growing demand from consumers for safer, healthier and more cost-effective nourishment and from policy makers, for new sustainable food and fish methods of production. What these issues have in common is a strong need to study the real-time development of complete living organisms, or parts of them – tissues, organs, cells, proteins, DNA, etc. Therefore, technologies for daily monitoring quality and process control are essential, as are rapid microbiological methods suited to the entire production system.

These drivers open the doors for a new biophotonics market, which is estimated to grow from $23 billion in 2012 to $36 billion by 2017. Photonic components – detectors, light engines, fibers, filters and other passive devices – are expected to reach an annual average growth rate of 8 percent. Looking in detail at the results of the study, the average growth varies from as high as 30 percent to as low as a few percentage points, depending on the application.

Figure 2a. Organic growth is one of four factors driving growth in biophotonics. Courtesy of Essilor.

What is behind these figures? We have identified four kinds of drivers:

• Organic growth, linked to the most mature market (x-ray imaging, vision care). The current target is 3 to 6 percent growth, an average between 0 and 2 percent in OECD countries and 10 and 20 percent in emerging countries.

• The increasing role of biophotonic components in medical, biological and agro devices. Examples: photoacoustic modalities for continuous enhancement of ultrasonic diagnostics; next-generation microscopes that offer phase information, polarization, superresolution and more; and future multimodal imaging techniques that combine optical and x-ray devices. The growth target could be around 15 to 20 percent, linked to both the existing market and any resistance from incumbent technologies that accompany and fund the development of photonic add-ons.

Figure 2b. Increasing photonics in end products is another factor driving biophotonics growth. Courtesy of Tematys.

• Replacing established technologies with biophotonic ones. Examples: direct optical detection or cytometry taking the place of petri boxes, the former gold standard, in pharmaceuticals, food, dairy and wine; optical biopsies versus histopathology; and photodynamic therapy versus chemotherapy in oncology. Here, growth is lower in the short- and midterm, and the risk is higher because of stronger resistance from incumbent technologies that can’t match with photonic ones.

• Emerging markets linked to the intrinsic nature of biophotonic technologies: sensitivity, accuracy, minimal invasiveness and real-time results. For example, fluorescence imaging prevailed in the past 15 years (LiCor, Caliper and others). Now optical in-line monitoring has taken over in the agro-food industry (Thermo, Bruker and others), and tomorrow, personal handheld spectroscopy will dominate. So far, this is the most unpredictable growth area because of nonestablished ways to appreciate the real value of the device and the most appropriate way to deliver it into the market.

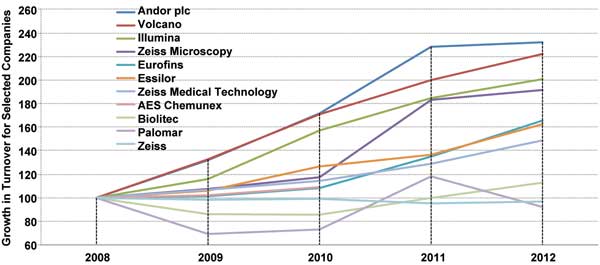

Emerging applications are granting market access to new players. The capacity of biophotonics to fuel companies’ growth is highlighted in Figure 3, gathering the growth rates of selected key players in the targeted markets. In the uglier years of deep global economic crisis (2008-2012), some of these companies saw more than 100 percent growth.

Figure 3. Compared growth of selected players in targeted markets (2008–2012). Sources: Annual reports from the companies; the base value in turnover was 100 in 2008. Courtesy of Tematys.

The stronger growth has mainly been found in analytics and sensing in the life sciences, pharmaceutical and agro markets – e.g., Illumina and Volcano in the US, Andor in the UK, Zeiss Microscopy in Germany and Eurofins in France. Key players in medical devices, such as Essilor and Zeiss Medical Technology, succeeded in average growth of 40 to 50 percent, thanks largely to the economic situations of consumers and states. Laser treatments – Biolitec of Germany, Palomar of the US, and others – were more affected by the crisis and have had more difficulty rebounding from it.

The technologies themselves are ready for wider deployment. Raman imaging and sensing, photoacoustic tomography and microscopy, handheld spectroscopy, terahertz imaging and others have benefited from huge telecommunications investments in sources, detectors and fibers; investments in storage led to advances in blue light. In the same way, solar investments will make available large-area sensors, light-trapping technologies and devices for fast online control, probably recyclable in vegetal and algae production. Once limited to hundreds or thousands of units per year in high-end desktop devices for life sciences and health care applications, biophotonics has the potential to be a part of increasingly rugged and cost-effective devices targeting million-unit markets – and to open doors for new entrants, continuing their migration from life sciences and health care applications to agro-food as well as environment control and monitoring.

Bringing medical care to a patient’s home requires relatively inexpensive and miniaturized tests – but they have to be sensitive, too. Biophotonics is therefore well positioned for home-care applications.

Private and public support are mandatory for small- and medium-size enterprises in biophotonics. As mentioned earlier, even if industrial issues have been addressed through telecom, solar, storage and other things, the entry barriers are high for biophotonic products; these barriers include R&D and product distribution.

From the R&D side, the young science of interactions between tissues and photons has yet to deal with the wide interdisciplinary fields of surface chemistry, micromechanical and fluidics engineering, needed to transform a light interaction into a valued product. The whole process implies numerous scientists, engineers, clinicians, technicians and shareholders; involves high-risk projects; and remains hard to manage during the complete 5- to 10-year cycle of science and product development, even if off-the-shelf components are now available. It will be important for the photonics community not to isolate itself in a bubble, but to engage more with medical doctors and surgeons; cluster organizations such as EPIC bring companies together and also help connect them with end users and the world at large.

From the product side, the markets served by biophotonics are highly regulated but jeopardized. If agro-food and water monitoring schemes are now regulated under European directives, the national protocols for benefit assessment and reimbursement schemes of a new therapy/medical device/diagnostic method have not yet reached a European common framework.

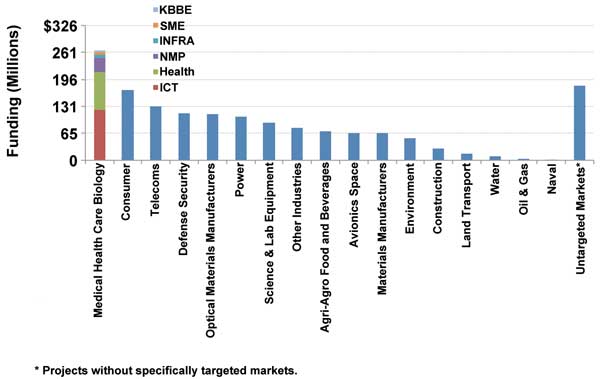

Figure 4. Distribution of photonics-related funding in the EU. Courtesy of Tematys.

And last but not least, clinical trials of new modalities – in plasmonics, photodynamic therapy, diffuse optical tomography, etc. – require money and time, and remain expensive tasks for undercapitalized companies. These three steps require national or supranational support for the challenging main phase and private support for the lengthy but less risky ones.

But the good news is that support is available. A survey of more than 5000 European Union programs funded between January 2007 and July 2012 under Framework Programme 7 revealed that budgets allocated to photonics in the first five years of FP7 represent €1.3 billion out of the overall €18 billion (about $23.5 billion) in funding for all programs (i.e., 7 percent of the global amount). Biophotonics is the highest-funded sector, with €260 million (i.e., 20 percent) invested in 72 R&D projects, twice the amount invested in competing technologies – telecom, defense, consumer applications, etc.

Looking into funded biophotonic technologies, 90 percent of the projects concerned health and the life sciences. Less than 10 percent are oriented toward the environment or food quality control; these accurate and real-time applications are growing up now and will replace “gold standard” methods in the next decade. After all, health spending is generally moving from treatment to diagnosis and monitoring.

The same trend is emphasized in FP7, where 81 percent of the whole funding is dedicated to diagnosis and monitoring. The investments in new minimally invasive therapies – photodynamics, endosurgery with lasers, optogenetics, etc. – are at the heart of the strategy.

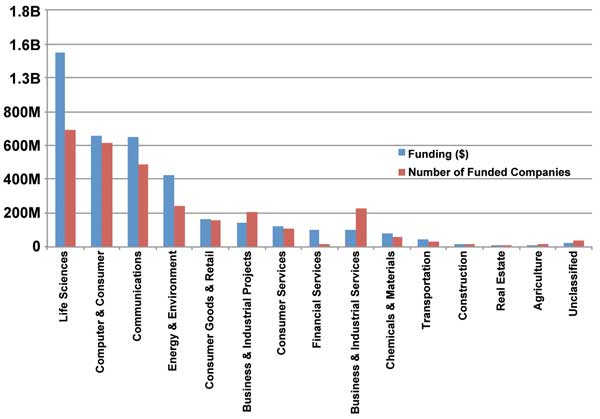

Concerning the launch and startup phase, the 2012 annual report of the European Venture Capital Association mentions that among 2966 venture capital-funded companies, 699 (about one-quarter) were active in the business of life sciences, making this sector the most funded in the early stage since 2008. Ventures are mainly in biotechnologies, but medical devices, medical equipment and drug development technologies – all strong integrators of biophotonics – represent one-third of the whole.

Figure 5. Life sciences enjoys a large lead over other fields in sector-focused investments (red bar) and is leading the pack in number of venture capital-funded companies. Source: Yearbook 2012 EVCA (European Private Equity and Venture Capital Association). Courtesy of Tematys.

What’s next?

Recently, large pharmaceutical companies have invested to fill the gap in the biotech industry: A year ago, GlaxoSmithKline and Johnson & Johnson announced the formation of a $200 million fund with a venture capital company to invest in early-stage life sciences companies. GSK and J&J will each invest $50 million to the new fund, while the VC will contribute $100 million. The new model allows the pharmaceutical companies to become acquainted with an asset as it is being developed, and the portfolio companies of the VC fund can gain the wisdom of the pharmaceutical industry early on in the process.

Key biophotonics players in the next 10 years could be either established ones – Philips, GE, Toshiba, Horiba, Thermo and others – or possibly newcomers well-suited to mass-market business models and industrial constraints – Samsung, Intel, Google, etc. Their financial and industrial commitment in such an early stage could be most useful.

Biophotonics is full of promise, and the best applications are still to come.

Meet the authors

Jacques Cochard is the founder of Tematys as well as a professor at École Polytechnique in France; email: [email protected]. Carlos Lee is director general at EPIC; email: [email protected].