RONALD MUELLER, VISION MARKETS

Meet the author

Ronald Mueller is an expert in the global machine vision industry, with a Ph.D. in computer vision and machine learning. Based on his technical know-how, his experience as a corporate executive, and his first-hand experience in machine vision sales in Europe, North America, and China, he founded the consulting firm Vision

Markets in 2014. He, his team, and the

Vision Markets Network of experts are

dedicated to making businesses thrive in this globalized growth market of machine vision; email: [email protected].

The machine vision market has gained enormous attention from investors, especially over the last three years after

the stock prices of several publicly listed vision companies began to skyrocket. At the same time, investors as well as

ambitious enterprises are no longer satisfied with growing a

company at the same rate as the market. When developing a corporate growth strategy, a detailed look at the specific value chain around a machine vision company often reveals interesting growth potential enabled by integrating up and/or down in the value chain.

The boon and bane of machine vision is its incredibly versatile arena of applications. Even though hundreds of thousands of companies use machine vision today, it’s still a complicated

technology. The level of know-how a customer possesses

dictates the level of integration required for a given application. This leads to a multistaged value chain that starts with OEMs

for basic components and extends all the way up to end users,

with several integrators and OEMs in between.

Skilled customers can design systems themselves and purchase components such as image-only cameras, lenses, lights, cables, and software. Those who have less machine vision acumen

often opt for systems in which the optical, electronic, and software elements are fully integrated. On the other end of the spectrum are factory operators who buy systems directly from production line builders where machine vision is integrated deep “under the hood.” For example, a large food producer would have an in-house team to develop its key vision-enhanced packaging machines. This food producer buys directly from component OEMs or distributors, while a small food producer asks for integrated vision systems or complete packaging machines from automation machine OEMs. Depending on the required level of integration needed, the price of the purchased products and services increases significantly.

Component OEMs sit at one end of the value chain, while device OEMs and end users sit at the other. Device OEMs often purchase cost-optimized machine vision components because of the targeted scale of their businesses. The need for tight integration in compact devices often calls for customization of standard components or dedicated developments.

The value chain between the end user and

the component OEMs of a vision-based

solution can be much longer, with usually

three players in between. As an example, the end user would task a large systems integrator to build a production line. This line builder purchases equipment from different machinery OEMs. In those machines, machine vision is just one enabling element, and the core competence of the OEM lies in other areas. Thus, this machinery OEM requires a machine vision systems integrator to develop a subsystem to be integrated into the final machine. Finally, the systems integrator gets his components from a component OEM or distributor.

The more you know, the more you DIY

Sooner or later, customers of vision-enhanced

systems realize the potential and the competitive

advantage that derives from machine vision.

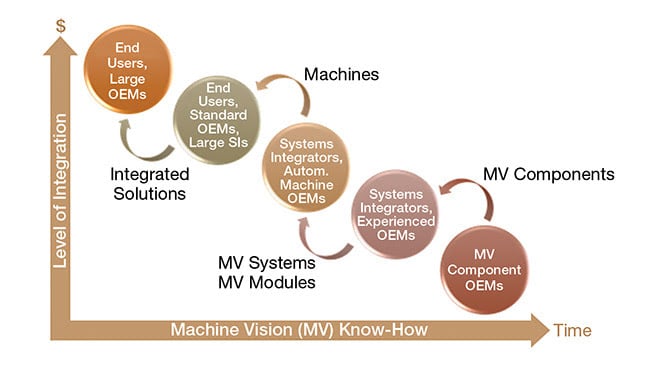

The vision markets chart (above, left) illustrates the accumulation of margins over the value chain from the component OEM over several integrators and intermediate modules or system OEMs. Motivated by the benefits of developing their own intellectual property and

bypassing the margin accumulation over the value chain, many customers integrate downward. On the end of the chain, device OEMs may develop their own camera modules and bring the component OEMs’ business in-house. Machinery OEMs learn how to spec, design, and integrate vision systems for their applications so they can buy directly from component OEMs. Even large end users start developing

their own standardized vision-based systems to optimize

their manufacturing lines with their own machine vision

intellectual property.

The position of a company versus its competitors, compared with its target customer groups in the areas of machine vision know-how and the level of integration/profit contribution. Courtesy of Vision Markets.

The process of gathering and using know-how in-house

obviously takes time, and this is why, in the chart, the X axis not only indicates know-how but also time. This means

OEMs and systems integrators are prone to losing customers over time because the customers start doing vision-based jobs internally. The good news is that there is an ever-refilling and growing funnel of customers who will start to use

machine vision technologies in their applications in the foreseeable future.

Where is the sweet spot?

The machine vision market as such is arbitrarily hard to

define. Independent of the definition, though, market studies

see high single-digit to low double-digit annual growth rates for the machine vision market. The largest players used to show a CAGR of well above 15% over previous years. If we believe the market studies, this indicates a much slower growth or even decline for the smaller players, so one might think the sweet spots are taken.

When customers of vision-enhanced systems realize the potential of machine vision for their businesses, and the

margin accumulation over the value chain, many start to integrate downward.

Each of the six business models listed (left) has different

characteristics of the opposing requirements on fixed costs, profit contribution, scalability, and defendability. When it comes to the optimization of profit contribution, however, the chart displays the potential for leaping over one or more levels in the value chain.

As described above, this happens when end users and

OEMs integrate downward in the value chain. But the same can happen in the other direction. For just one example,

component OEMs can achieve attractive profit contributions well above 65% if they bundle several hardware components with software licenses as enabling subsystems to machinery OEMs. If an OEM also handles the mechanics, such as when the position of lighting and optics are critical, even higher turnover at the same profit contribution is possible.

Yet the overall value of a company and its business model also depends on scalability. If such productized subsystems can serve a large target market, or if they are highly

competitive in an attractive niche market, the requirement

of scalability is also met. On the other hand, the more

that customization and integration work are involved, the higher the defendability. But more so, the scalability is limited by the available engineering and sales resources.

For the design or evaluation of a business strategy, the chart depicts the position of a company versus its competitors,

versus its target customer groups in the dimensions of machine vision know-how/time and level of integration/profit contribution. Ideally, the profit contribution on the Y axis and also the time on the X axis should be quantified depending on the scenario in focus. The market value or the number of accounts in a target customer group can be indicated by the size of the circle. Once completed, the chart depicts the technology strengths and weaknesses as well as the market opportunities and threads of a business model.

Each of the abovementioned business models, which can also be seen as customer groups, has different requirements beyond the level of integration, such as ease of use, technical support, cost, availability, and innovation. In a later column, we will introduce a way to prioritize the requirements of all target customer groups quantitatively. This will allow you to measure how well your offerings and your market positioning meet the needs of your target markets.

Links in the Chain

There are essentially six types of business models in the

vision value chain that reflect the levels of product

integration and machine vision know-how.

Component OEMs — OEMs of machine vision components including cameras lenses, optics, lights, cables, software libraries, and accessories. Though on a higher level of

integration, OEMs of smart cameras and code readers also fall into this category.

Device OEMs — OEMs of devices designed to fulfill a certain purpose and operating widely as stand-alone units sold

in the many hundreds or thousands, such as blood

analyzers, measurement projectors, or mobile code

scanners for delivery services.

Machinery OEMs — OEMs of larger machines for use as stand-alone units or fully integrated into production lines and sold in the several dozens or hundreds. Examples include automatic optical inspection (AOI) machines

for assembled printed circuit boards, screw inspection machines, or universal and vision-enhanced robot cells

for pick-and-place tasks.

|

End Users — A variety of customers across numerous

industries. Examples range from an OEM purchasing vision-enhanced machines or full production lines to

soccer league associations equipping their stadiums

with goal cameras.

Systems Integrators — Companies developing highly

customized solutions for OEMs or end users, from

complete production lines down to modules comprising few components, software algorithms, and hardware/

software interfaces that are sold just once or a couple

of times. Mostly small companies with local reach.

Distributors — Resellers usually supporting a selection of compatible machine vision components.

|