As the automotive lidar industry sets goals for reaching full autonomy, venture capital investment in transportation shows no signs of slowing.

GREG SMOLKA, INSIGHT LIDAR

As society considers a future with

autonomous vehicles (AVs), lidar continues to be a hot topic. Since 2016, there has been huge interest in automotive lidar, which has resulted in investments and advancements in transportation and other lidar applications. The following snapshot combines ground-level insights (from the Brussels AutoSens and Michigan Automotive LIDAR conferences) with reports from industry analysts, and offers a look into the current state of the automotive lidar industry.

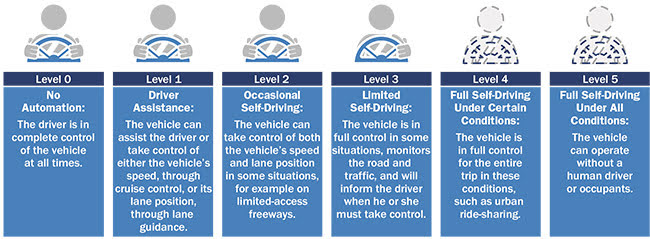

There’s no doubt that the vehicles hitting the roads today are smarter than ever before, but full automation is still in the future. To understand the path toward fully self-driving vehicles, it’s useful to know the six levels of autonomous driving, as defined by the Society of Automotive Engineers (SAE) (Figure 1). The levels are:

- Level 0: No Automation.

- Level 1: Driver Assistance.

- Level 2: Partial Automation.

- Level 3: Conditional Automation.

- Level 4: High Automation.

- Level 5: Full Automation.

Although lidar has been incorporated into some existing L2/L3 vehicles, it is seen as critical for L4/L5 operation. Except for Tesla, all major OEMs believe lidar is required. Speaking at AutoSens, Dexin Chen, senior analyst at IHS Markit, quoted BMW’s chief technology officer, Klaus Fröhlich: “Lidar is a strict requirement for L3 at 130 kph [80 mph]. Detection of 9-cm obstacles at 150 meters at 130 kph is impossible without it.” At Automotive LIDAR, Mike Pinelis, president and CEO of Microtech Ventures Inc., echoed Fröhlich, noting, “Most tier ones and OEMs believe that lidar is necessary and very important.”

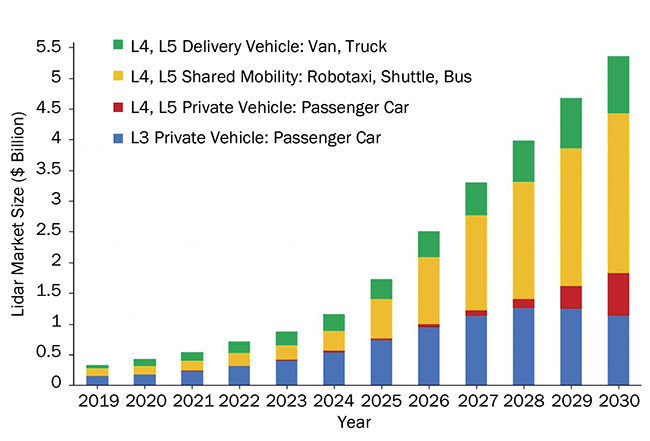

This criticality drives an active and fast-growing market. Research from IHS Markit shows anywhere from 80 to 100 companies working in automotive lidar. Basic systems, which essentially act as precollision sensors, dominate today’s lidar shipments (around 4 million units per year). However, IHS predicts strong growth in higher-capability lidar as more ADASs (advanced driver-assisted systems) and fully autonomous vehicles are deployed. The company sees the automotive lidar market growing to nearly 18 million units by 2025. Similarly, Nilushi Wijeyasinghe, technology analyst at IDTechEx Ltd., sees strong growth in the automotive 3D lidar market, with revenue growing at a compound annual growth rate (CAGR) of 29%, to $5.4 billion by 2030 (Figure 2).

Figure 1. SAE International J3016_201806: Taxonomy and Definitions for Terms Related to Driving Automation Systems for On-Road Motor Vehicles (Warrendale, Pa.: SAE International, June 15, 2018), www.sae.org/standards/content/j3016_201806. Courtesy of SAE (Society of Automotive Engineers) and NHTSA (National Highway Traffic Safety Administration).

Waymo, Cruise, and ridesharing services such as Uber and Lyft have been testing self-driving capabilities, and L4/L5 self-driving is expected to be adopted by robotaxis before personal vehicle adoption. Initial deployments are planned to roll out over the next few years.

Market movement

According to IDTechEx, as of August, $1.9 billion was invested in the 2019 lidar market. PitchBook’s third quarter 2019 Mobility Tech report shows that the lidar industry was on track for a record year, with approximately $1.2 billion in venture capital (VC) investment in the first three quarters of the year. Since 2009, investors have deployed over $2.5 billion in VC dollars into the industry. PitchBook analyst Asad Hussain said, “Lidar is one of the main growth areas in terms of VC dollars flowing into the mobility and transportation industry. There are a multitude of new players and emerging technologies in the space. We see great opportunities for early investors. New, smaller companies are entering the market with technologies that are higher performance and could radically reduce the cost of lidar.” Companies that have established themselves within the market are protecting their technologies with patent enforcement. One company has already sued two rivals for infringement.

Various technologies

Various lidar technologies are being developed to address the needs of the AV market, generally categorized by detection technique, scanning technique, and laser source.

Detection techniques include time of flight (TOF) or frequency-modulated continuous wave (FMCW). TOF lidar images by sending out a short light pulse and then measuring the time it takes for a reflection to return. Only a small amount of light reaches the receiver, meaning sensitive detectors are required. Most of these current systems use lasers that operate at around 905 nm. Short-pulse lasers and sensitive detectors are available at this wavelength. However, there is a limit to the amount of laser power that can be delivered while remaining human eye safe. This eye-safe limit makes it difficult for the current generation of lidar to reach the 200-m range requirement desired for use in self-driving applications. Some companies are developing systems that operate at 1550 nm, allowing for more eye-safe power, thus longer range, but the systems require more expensive laser and detector components.

Figure 2. Projected growth in the 3D lidar market between 2019 and 2030. Courtesy of IDTechEx.

FMCW lidar is emerging as a promising alternative detection technique that helps overcome the existing range problem and adds additional measurement capability while offering the promise of low-cost chip-scale integration (Figure 3). FMCW lidar transmits a continuous beam of laser light, sweeping through a range of wavelengths. Similar to TOF sensors, FMCW lidar looks for the signal reflected from an object. However, it compares the frequency of the reflection to a local copy of the transmitted signal. The difference in frequency is used to determine the range. Importantly, when the return signal is combined with the local copy, the signal is amplified by 10 to 1000×, enabling much more sensitive detection. This process, analogous to how automotive radar works, is called coherent detection and allows FMCW lidars to recognize faint objects at a greater distance.

Lidar scanning techniques include mechanical (spinning, galvo mirrors, polygons, or MEMS), solid-state (flash or optoelectronic pulse amplifiers), and hybrid. The spinning technique mounts lasers onto a rotating gimbal. Galvos, polygons, and MEMS all use moving optical elements to scan a scene. Solid-state lidar uses no moving parts to paint a scene, offering high reliability but typically limited range or resolution. Hybrid systems include a combination of scanning methods.

Figure 3. Widespread development depends on low-cost, long-range, chip-scale lidar. Courtesy of Insight LiDAR.

The real challenge for automotive lidar is meeting the list of L4/L5 autonomy requirements simultaneously. These are:

Range

To ensure passenger and pedestrian safety, AVs must be able to detect and identify objects at a distance of 200 to 250 m. Think about it this way: A vehicle traveling 65 mph covers 200 m in about 7 s. The vehicle needs to be able to detect and identify an object, say a small child in a dark coat, and have enough time to decide how to react.

Sensitivity

Different materials in the environment reflect various amounts of light. For example, a white car may have a reflectivity of 40%, while a glossy black car reflects only 4%. Thus, it’s essential to describe the range and also the reflectivity of the objects at that range. Lidars for AVs need to detect a 10%-reflectivity target 200 m away.

Resolution

Cameras typically specify resolution in megapixels. Lidar typically specifies resolution by describing the angular spacing between pixels. Current-generation lidar sensors typically have a resolution of 0.2° × 0.1° (vertical × horizontal), with some systems as high as 0.1° × 0.1°. While this is adequate for shorter ranges (<100 m), long-range lidar (up to 250 m) needs better resolution, as much as 0.025° × 0.025°.

Frame rate

Lidars for AVs need a frame rate of

at least 10 fps, with a rate of 20 fps or more being desirable. A higher frame rate typically means faster decisions by the AV.

Fields of view

AVs need to see the world around them, thus full horizontal 360° FOV is necessary. AV manufacturers accomplish this by either placing a rotational lidar on top of the vehicle or by placing multiple lidars at different locations on the vehicle. The goal is to minimize the number of lidars per vehicle, while still achieving 360° vision. Vertical FOV is typically 30° to 40°.

Immunity

Lidar sensors have to operate in bright sunlight or at night without their performance being affected. They also have to be able to work while other lidars are operating nearby. Traditional lidar addresses this issue with optical filters and pulse-encoding schemes. The new generation of FMCW lidar is naturally immune to such signals because of its detection technique.

Velocity measurement

To determine which objects to track and avoid, AVs need to determine the velocity of objects in their path. With traditional lidar sensors, velocity is calculated by taking a number of range calculations over time, then calculating how fast the object is moving. This method can be effective, but can also be error-prone and time-consuming. The new generation of FMCW lidar captures the velocity of objects with a single measurement, enabling much faster decisions, which are critical when the AV or external objects are moving at high speeds, or when difficult maneuvers are required.

Cost

These performance goals must be met, and they must be met at low cost to enable widespread deployment. OEMs are looking for lidar sensors that cost less than $250 in high volume.

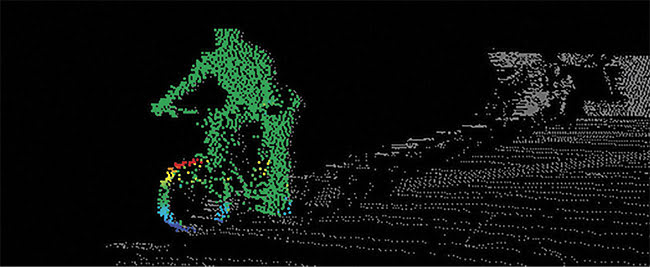

Figure 4. FMCW detection adds instantaneous velocity measurement for faster AV decisions. Courtesy of Insight LiDAR.

Six key trends

1. Longer range, higher resolution

Autonomy requires quick and accurate decision-making in many different conditions (Figure 4). Challenging conditions include unprotected left turns and debris on the road. Wijeyasinghe of IDTechEx expects the automotive industry to shift toward FMCW over the next decade because of the technique’s longer-range capabilities and its ability to directly detect velocity. “IDTechEx has identified 16 automotive tier-two companies developing FMCW lidar, and also had discussions with automotive OEMs who are interested in this next-generation technology,” she said. FMCW is more sensitive overall, is immune to sunlight and other lidar, and offers direct velocity in every pixel. TOF solutions are approaching the range challenge by using shorter pulse widths and more sensitive detectors.

2. Mechanical scanning

Solid-state scanning solutions are highly desired because of perceived reliability gains, and they have not yet achieved the required performance for L4/L5 AVs. Hybrid solid-state and mechanical solutions are driving significant interest in the market, though meeting all of the performance and cost specs simultaneously is still critical. Ultimately, the prevailing AV lidar technology will have to be automotive qualified and

ultrarugged. (Note: MEMS lidar cannot be classified as solid state because it contains small moving parts.)

3. Specification standardization

At least two companies in the field have come out in favor of new measures to quantify lidar performance. Standard specifications are aimed at helping compare all lidar options on the same scale to determine the best options for use in AVs. Although attractive in theory, standardization may be hard to achieve since it is not as simple as specifying just range and reflectivity. Some specifications will differ based on detection technique.

The probability of detection, false-alarm rate, refresh rate, field of view, solar load, signals from other lidar, and many other factors are important to consider when attempting to standardize specs in the industry.

It can be difficult for OEMs to evaluate the various technologies without standardization. For example, one company may specify detection at 200 m at a 10% target but with a narrow field of vision, it may not specify frame rate or pixel density at all, or its specifications may be developed for nighttime when solar background doesn’t affect detectors. It is necessary for OEMs to comprehend the full range of specifications and conditions to understand how sensors are likely to perform.

Although attractive, standardization is not likely to be resolved until one technology emerges within the industry as the default. Lidar has so many technologies, configurations, and measurement methods (while radar and cameras do not), which makes the journey toward standardization a long one.

4. Cost and AV adoption

Cost will be a significant driver for adoption, especially for personal vehicles. Initial test vehicles featured expensive sensor suites. Early lidar systems cost $75,000 or more. While prices have dropped, the lidar used in today’s ADASs and AVs is still expensive, with price tags of $4000 to $8000 per unit. With multiple lidar units needed per vehicle, this is still too expensive for widespread deployment. Broad adoption will require lidar sensors that cost less than $250 per unit in high volume.

According to Chen in his AutoSens talk, “The Race to a Low-Cost Lidar System,” it is unclear whether any of the existing TOF technologies will be able to make it to the $250 price point. Chip-scale FMCW lidar, which is built using semiconductor processes, is likely required for meeting cost and performance targets for long-range lidar.

5. Multiple solutions

Short-range lidar could be used to ensure full close-in coverage around the AV. Long-range lidar will likely be incorporated to ensure safe L4/L5 operation at various speeds and under varying conditions.

6. Consolidation

With 100 or so players in the market,

many offering similar technology, consolidation is bound to happen. Chen said we’ve begun to see an uptick in mergers

and acquisitions for lidar makers.

Ultimately, those that prevail will have the ability to meet all of the specifications necessary for L4/L5 AVs, including cost targets. The vast majority of companies working on automotive lidar are also pursuing other applications such as

security, mapping, and industrial automation. While the automotive lidar market may consolidate, technological advancements driven by this market will have far-reaching effects.

Automotive lidar is emerging as one of the most exciting photonics applications in recent history, with its ability to positively affect millions of lives each year. Early deployments show the promise of the technology, while also highlighting the challenges that lie ahead for the industry in terms of range, resolutions, object detection, and cost. As the important work toward standardization progresses, efficient comparison of different lidar technologies will become possible.

Chip-scale FMCW lidar is emerging as a promising technique that enables long-range, high-resolution performance at industry cost targets.

Meet the author

Greg Smolka is vice president of business development at Insight LiDAR, where he focuses on building partnerships in the autonomous vehicle market. Previously, Smolka has guided photonics applications in biomedical imaging, semiconductors, telecommunications, and defense.