A recent study examines changes in manufacturing, business partnering, technology advancement and government incentives for the photovoltaics industry.

Anne L. Fischer, Senior Editor

It is no secret that the growth in solar technologies will greatly affect energy use, but it also is creating a shortage of silicon.

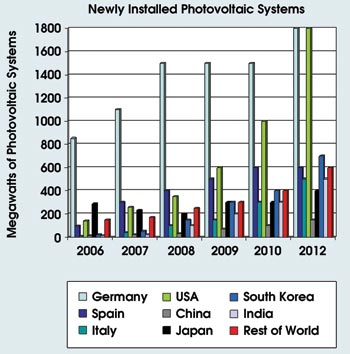

Spurring the growth in the solar market are government mandates to reduce dependence on fossil fuels, to reduce carbon emissions and to increase overall energy efficiencies. Another motivation, according to the presentation “Understanding Photovoltaics — from Raw Materials to Systems,” presented at the iSuppli European briefing in April by iSuppli of El Segundo, Calif., is feed-in tariffs, which are federal incentives that governments give to the owners of photovoltaic systems for feeding solar energy into the electrical grid. The German feed-in law has had a pronounced effect on the rate of solar growth (Figure 1). According to the law, every photovoltaic system must be connected to the grid, and every kilowatt hour must be purchased by the electric utility. The result expected by the German Solar Industry Association is grid-parity by 2018.

Figure 1. Germany is and will continue to be the largest regional photovoltaics market — it experienced profound growth in 2004 when the feed-in tariff law was revised and became mandatory. Photovoltaics in the US is expected to take off in 2009. Source: German Solar Industry Association.

The iSuppli study forecasts that by 2020, about 50,000 MW worth of photovoltaic systems (MWp) will be installed annually, up from 2,538 MWp in 2007, an increase of nearly 20 times. This translates to a global revenue of as much as $22.1 billion in 2012, up from $9.6 billion in 2007.

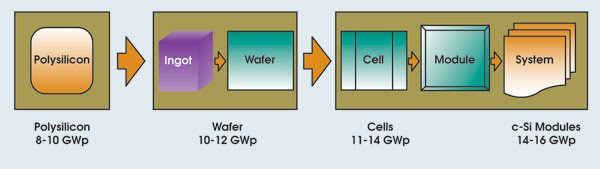

All this growth, however, is straining current supplies of polysilicon. It is forecast that in 2010, the photovoltaics industry will have the potential to manufacture cells and modules with production capacity of up to 14 GW worth of photovoltaic (GWp) systems, whereas there will be only enough silicon to produce 8 to 10 GWp (Figure 2).

Figure 2. The polysilicon supply will not match photovoltaic production capacity by the end of 2010. Source: European Photovoltaic Industry Association.

Silicon pricing

The shortage, not surprisingly, is driving up prices, according to Henning Wicht, senior director and principal analyst for microelectromechanical systems and photovoltaics for iSuppli. Polysilicon suppliers are demanding 10 to 20 percent of their total contract costs up front, which puts added pressure on photovoltaics manufacturers.

As a result, photovoltaics companies such as SolarWorld AG of Bonn, Germany, are partnering with chemical manufacturers such as Evonik Industries AG of Essen, Germany, to produce silicon expressly for solar use. Solar-grade silicon does not fulfill the requirements of electronic-grade silicon in terms of purity. The advantage, however, is that it is produced at lower cost.

Thin-film technologies are experiencing growth as a result of the silicon shortage. This is largely due to the fact that thin-film layers for photovoltaic cells can be conducted on glass, steel or polymer foils, without any — or with only a small percentage of — silicon.

Silicon cell manufacturers are increasingly investing in thin-film technologies in parallel with polysilicon. Materials include amorphous silicon (a-Si), which uses just 1/10 the amount of silicon in crystalline silicon (c-Si), and cadmium telluride (CdTe) and copper-indium-gallium-selenium intermetallic compound, Cu(In,Ga)Se2 (also known as CIS/CIGS), which are silicon-free and abundant.

Thin-film solar cells are less efficient than c-Si (with a convergence efficiency of 6 to 11 percent compared with 15 to 17 percent of c-Si), yet they are less expensive to produce. The production cost per watt is key in the energy industry and, therefore, the market for thin-film solar cells is expected to grow at an annual rate of 70 percent to gain a 20 percent market share by 2010. The cells will be used in high-volume applications, such as solar farms with more than 1-MW power generation, according to Wicht.

Energy cost

Despite the increased energy production from solar technologies, prices still are high for the end user. In Germany, for example, the cost for electricity generated by fossil fuels is about 20 cents per kilowatt hour compared with photovoltaic electricity, which is 30 to 50 cents per kilowatt hour. To drive photovoltaics costs down, solar companies are cutting costs across the supply chain, which includes materials, cells, modules and finished systems.

Q-Cells of Bitterfeld-Wolfen, Germany, for example, has indicated that it intends to reduce photovoltaic system costs by as much as 50 percent between 2007 and 2010. To cut these costs, companies will invest in different suppliers, they will scale up production and increase efficiency, and they will develop and adhere to production standards.

To increase production, Wicht contends that governments will have to maintain or set up incentives. However, many countries are revising or adapting the frameworks they have in place to reduce support. Or, even worse, some countries, such as China, are projected to have no government support in the foreseeable future. Germany is reviewing its feed-in tariffs for 2009 and beyond. Spain, which receives 50 to 100 percent more irradiation (sunlight) than Germany, expects to reduce its feed-in tariffs. The US government’s tax incentives end in December of this year.

To stimulate increased support, Wicht recommends that industries focus on reducing costs and turning out high-quality products with the promise of long-term use. This will motivate investors as well as national governments to support energy production from this most unfailing source.