An analysis of worldwide data reveals the potential for growth in mature and new technologies.

Arpad A. Bergh, Optoelectronics Industry Development Association

Optoelectronics is at the crossroads of electronics and optics. Using optical and electronic means, it generates, manipulates and converts light. Photonic devices process, store, transmit and display information for applications such as communications, displays, imaging, memory, biophotonics, energy generation and lighting. Photonics is an essential part of a country’s information infrastructure, which, in turn, plays a key role in its domestic economy and national defense.

The purpose of this article is to explore applications of optoelectronics, with an emphasis on their commercial significance. This is not a technology review, but rather a look at the commercial impact of mature and emerging optoelectronics technologies.

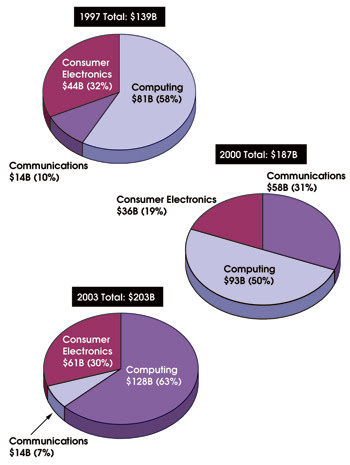

Figure 1. Worldwide optoelectronics markets have expanded relatively steadily from 1997 to 2003, despite the experience of a distinct “bubble” in the communications sector during this period. Source: Optoelectronics Industry Development Association market reports.

Market trends

The Optoelectronics Industry Development Association has kept track of the worldwide optoelectronics market for the past seven years. The relative market share of the major sectors — computing, consumer electronics and communications — is shown for 1997, 2000 and 2003 in Figure 1. Notice that the overall market steadily increased: from $139 billion in 1997 to $203 billion in 2003. The relative position of the communications sector, however, did not follow such a steady course. The 10 percent market share of communications in 1997 exploded to 31 percent in 2000 — and collapsed back to 7 percent in 2003.

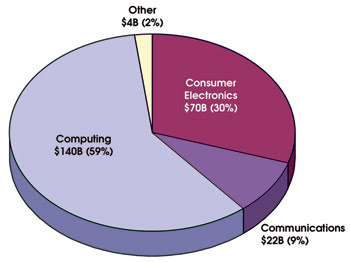

The local impact of the burst of the communications bubble depended on the optoelectronics portfolio in each country. In the US, communications dominated optoelectronics, and the burst had a devastating effect. Although significant, the impact was much less severe in the Pacific Rim, where a much greater emphasis had been placed on consumer electronics. By 2004, the worldwide optoelectronics market had grown to $236 billion (Figure 2).

Figure 2. Worldwide optoelectronics markets grew to $236 billion in 2004. Source: 2004 Optoelectronics Industry Development Association market report.

A trend involving the distinction among the three major application areas has emerged. In the past, each area had its own publications, trade shows and industry associations. In more recent years, however, the boundaries separating those areas have been blurring. For example, at the 2004 and 2005 International CES consumer electronics shows, an equal number of keynote speakers represented consumer electronics (Panasonic, Microsoft), computers (Intel, Hewlett-Packard) and communications (Verizon, SBC).

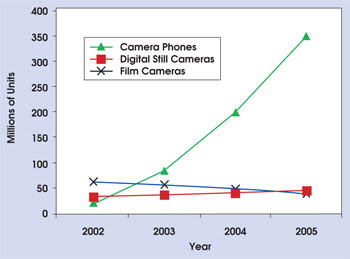

The merger of consumer electronics and communications is apparent in the incorporation of digital cameras into cell phones (Figure 3). Sales of camera phones in 2005 were expected to be seven times those of still cameras.

Figure 3. Worldwide camera sales have risen dramatically for camera phones, but less rapidly for stand-alone still cameras. Sources: Strategy Analytics, Optoelectronics Industry Development Association market reports and InfoTrends.

Mature areas

Although computers, consumer electronics and communications are relatively mature areas of optoelectronics, they are by no means stagnant. A steady stream of improvements appears in all segments.

For example, the largest market share currently belongs to flat panel displays, dominated by LCDs with a yearly volume of $39 billion. This technology was invented at RCA Corp.’s David Sarnoff Research Center in 1964. RCA revealed the technology in 1968 as the future of TV sets but declined to invest in it. Japanese companies picked it up, and today practically all flat panel display production is carried out in the Pacific Rim (Figure 4).

Figure 4. Virtually all LCD production takes place in the Pacific Rim. Source: Optoelectronics Industry Development Association market report.

The history of the LCD carries a lesson for believers in the current idea that innovation is the cornerstone of a nation’s industrial competitiveness, without regard for commercialization. What did the US get out of this technological development? Corning Corp. built several factories in the Far East to supply cover glasses for the displays, and George H. Heilmeier won the 2005 Kyoto Prize in Advanced Technology for his invention of the LCD at RCA.

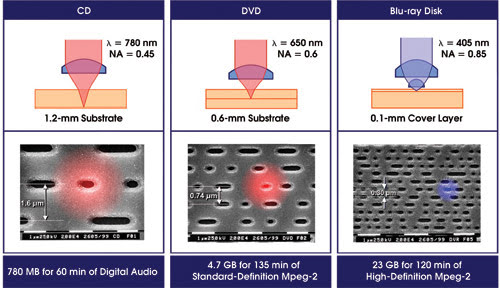

Another example of new developments in a mature area involves optical storage. The evolution of optical storage is guided by a decreasing spot size, enabled by decreasing the wavelength of the recording laser beam. The size of a focused laser beam is limited by diffraction to a spot on the order of the wavelength. Hence, the storage density of optical storage devices is inversely proportional to the square of the laser wavelength.

In CD and DVD players, infrared lasers are beamed onto the spinning disk, where they “read” a pattern of microscopic pits that represent the ones and zeros of digital data. Replacing the infrared laser with a shorter-wavelength alternative allows much smaller pits and, consequently, much more data per disk.

As the wavelength was reduced from the infrared of CDs to the red used in DVDs, storage capacity increased by almost an order of magnitude. The 650-MB-per-side storage capacity of the CD offered an ideal medium for music and voice, but it could not accommodate a full-length movie. Hence, the DVD was developed with a capacity of 4.7 GB per side, and it quickly became a commercial success, surpassing the growth of CDs.

The demand for data storage, however, is insatiable; no sooner had a solution been found for recording movies on DVDs than the media industry signaled the move to digital and high-resolution TV. To accommodate this development, a short-wavelength (405 nm) blue-violet semiconductor laser was constructed that can produce a beam one-fifth the size of the red lasers used in DVD players. This means that the blue laser can read much smaller bits of information on a disk, allowing more data to be stored on it. The three generations of optical storage technologies are shown in Figure 5.

Figure 5. Optical storage densities have increased significantly with the evolution of CD, DVD and Blu-ray technologies.

The origins of the Blu-ray optical storage standard, which incorporates these short-wavelength lasers, can be traced back to 1993, but it was only in February 2002 that nine audiovisual producers — Hitachi, LG Electronics, Matsushita (Panasonic), Pioneer, Philips, Samsung, Sharp, Thomson and Sony — joined forces to develop a larger-capacity disk capable of recording more than two hours of digital high-definition video. Sony launched the first Blu-ray DVD recorder in Japan in April 2003.

There is a fly in the ointment, however, for the companies supporting Blu-ray. Other high-definition DVD rivals are trying to capture the lucrative licensing royalties that come from inventing a successful format. The main challengers are Toshiba and NEC, which are collaborating to develop an alternative technology called Advanced Optical Disc. The advantage of this approach is its compatibility with the current DVD encoding system and that, unlike Blu-ray, it can be readily made in existing DVD plants.

The potential competition for Blu-ray does not end with the Advanced Optical Disc. Other rivals include Sanyo and a Chinese recording system called Enhanced Versatile Disc. Sanyo, which is not part of the Blu-ray grouping, has a superior blue laser and is developing a laser format expected to fit 54 GB per side, compared with the 27-GB disk capacity of Blu-ray. To avoid the royalty demands of DVD rights-holders, an Advanced Optical Storage Research Consortium was set up in 2002 by manufacturers on both sides of the Taiwan Strait, with the aim of developing the Enhanced Versatile Disc as the sole optical storage standard to be used in the China region.

The lack of international industry standards offers a lesson regarding the importance of the optoelectronics infrastructure. This lack of standards can waste enormous amounts of development funds and delay the introduction of new products. It is not clear yet which of the high-density DVD formats will dominate the market, but it is quite clear that high-definition DVD will generate a great demand for blue lasers.

There is no room here to elaborate on all of the evolving technologies related to communications, computing and consumer electronics. Suffice it to mention that ongoing development is occurring in specialty fibers, imaging, LED projectors, organic LEDs, flexible 3-D displays, fiber-to-the-premises connectivity and optical storage.

Several promising areas of application for optoelectronic devices include optical interconnects, LED lighting and illumination, optical sensors and solar cells. In most of these, optoelectronic devices replace other technology, usually electronics. Hence, they must outshine the current devices in performance, cost and reliability. This is a tall order, especially with regard to cost, because low costs require high-volume production that is difficult to achieve without international standards.

Interconnects. Optical technology has displaced copper wiring in longer-distance telecommunications as well as in many enterprise networking applications. However, there has been no commercially viable implementation of optical interconnects for short-distance, box-to-box links of less than 10 m.

Progress has been made in replacing short-distance electronic interconnects with optical ones (see Photonics Spectra, November, pages 52-74). Doing so entails implementing the functionalities of photonics in silicon, the fundamental building material of electronic devices. The technology of silicon photonics is being pursued in many laboratories around the world.

New technology is introduced into silicon fabrication plants on a four-year cycle. The challenge today is to develop silicon photonics technology by 2008 so that its introduction into production lines can be scheduled for 2012.

LEDs. LED sources are used increasingly in two applications: direct-view lighting, such as an indicator, display or traffic light, and reflected-light applications, such as general indoor and outdoor illumination.

In monochrome applications, LEDs have established a substantial market. They outperform conventional light sources in efficiency, lifetime, compactness and ruggedness. They can be used in indicator lights, signage, traffic signals, buildings and furniture. In all these applications, LEDs provide a new lighting paradigm. Their small size, low voltage and long life make it feasible to build them into furniture or other appliances. In fact, the largest market for high-brightness LEDs is in mobile appliances such as cell phones, digital personal assistants and cameras.

Improved LED efficiency

Over the past decade, LED efficiency has steadily improved until it exceeds that of incandescent lamps, the most inefficient general source of light. If this progress continues, LEDs also will outperform fluorescent lamps and will be contenders to become the primary source for general illumination, representing a $40 billion market worldwide.

The ideal LED light source for such applications is a multicolor (red, green and blue) lamp with high efficiency, long life, adjustable color and brightness. It would be controlled by a CMOS circuit to provide the proper illumination for any occasion at a competitive cost. A major development effort will be required to make such devices cost-effective in comparison with conventional sources, but the energy savings should justify the effort.

Such a white lamp with an efficiency of 150 to 200 lm/W will remain a challenging and worthwhile target for many years. Problems that must be solved include:

• The different efficiency, voltage, temperature dependence and rate of degradation of the various colors of LEDs.

• The lack of high efficiency, where luminous efficacy (lumens/watt) is the highest of all colors of LEDs (especially those emitting in the yellow/green).

• The challenges involved in achieving efficient, low-cost color mixing and light distribution.

Hence, LEDs likely first will move into niche markets in general illumination, such as architectural lights and furniture lighting.

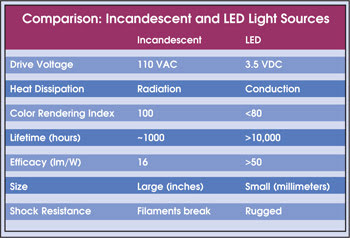

Even if LEDs achieve the necessary cost reductions and improved efficiencies, they must cross other hurdles before they can be used for general illumination, as shown by comparing state-of-the-art LEDs and conventional incandescent lighting (see table). In replacing incandescent lights, the first three parameters — drive voltage, heat dissipation and color rendering index — do not favor LEDs. They require a different power supply, and so carry the inherent loss of down-conversion when attached to the 110-V power grid. They must be mounted on a heat sink because they dissipate heat by conduction, and they have a low color rendering index value.

On the other hand, LEDs have some unique attributes, as shown by their relative lifetime, efficacy, size and shock resistance. Their long life, ruggedness and high efficacy render them ideal light sources for mobile platforms.

On the other hand, LEDs have some unique attributes, as shown by their relative lifetime, efficacy, size and shock resistance. Their long life, ruggedness and high efficacy render them ideal light sources for mobile platforms.

It is expected that LEDs eventually will provide all interior and exterior automotive lighting. They offer several advantages, such as low radiated heat, small size, high reliability and ease of manufacture, that translate to low costs. Similar opportunities will emerge for LEDs in other mobile platforms, such as airplanes, ships and trains.

LED lighting represents a major paradigm shift. Those who look for one-on-one replacement for traditional sources will fail. Those who look for new lighting solutions, including powering, fixtures, controls and intelligence, will succeed.

To define optimum conditions, major field experiments are needed, such as those in progress in Japan, South Korea and Taiwan with government support. An experiment in South Korea, for example, involves the installation of LED lighting in three city blocks, including highways, a bridge and many buildings.

Optical sensors. Semiconductor lasers and LEDs play an important role in defense and in environmental control as biological-agent sensors for toxin detection and pollution monitoring. A variety of natural substances can be detected and identified through laser-induced fluorescence, and others can be “tagged” through the excitation of fluorescent dyes and proteins. Laser-induced fluorescence also will provide a powerful diagnostic tool in identifying the molecular signatures of cancer and other diseases.

The natural evolution of the Information Age leads to the increasing use of intelligent systems in applications ranging from traffic monitoring and pollution control to security and structural maintenance. The key element in any intelligent system is reliable input, for which good sensors are required.

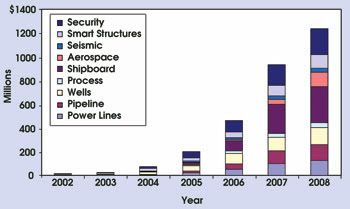

The worldwide sensors market is approximately $50 billion per year (Figure 6). Optoelectronic sensors are making rapid inroads for many applications where they are unique, such as image sensors in digital cameras, and where they provide better performance and resistance to harsh environments.

Figure 6. The market for optical sensors has grown dramatically in recent years. Note that automotive and medical sensors are not included here. Source: D. Krohn, Light Wave Venture.

The sensor technologies and their applications include:

• Bragg gratings (distributive point sensors) for temperature, strain and pressure sensing.

• Raman scattering (distributive continuous sensors) for temperature and other sensing.

• Sagnac interferometers for gyroscopes.

• Brillouin scattering for temperature and strain sensing.

• Fluorescence for the sensing of chemicals.

• Microbending for temperature and strain sensing.

• Microresonators for temperature, strain and chemical sensing.

The need for sensors is widespread and includes many security, defense, medical, biotechnological and industrial applications. The success of the sensor industry will depend on the ability to develop international standards and achieve multiple-use applications.

Solar cells. Although the technology behind the solar cell is not new, the changing economic environment is. As oil prices increase, and as the awareness grows of the need to create a cleaner environment, solar cells are becoming more attractive. They are especially embraced in Germany, Japan and Taiwan and are supported by government initiatives.

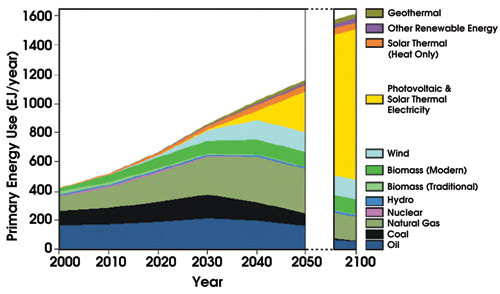

Long-range predictions of the contribution of solar cells to the generation of electricity in this century are shown in Figure 7, as envisioned in Germany.

Figure 7. Solar energy is expected to play an increasing role in meeting nations’ energy needs. These data show projections for Germany. Source: Germany Advisory Council, 2003.

Summary

Taking a broad view of optoelectronic applications, the following conclusions can be drawn. Optoelectronics is still a vibrant, emerging technology with a bright future. Countries that can capitalize on this opportunity maintain diversified portfolios and have strong industry/government partnerships. The US is strong in the areas of invention — e.g., LCD displays — but weak in commercialization. The largest optoelectronics market is in flat panel displays, invented in the US but produced exclusively in the Pacific Rim. Finally, in areas where optoelectronics technology penetrates existing markets, a systematic approach is needed to demonstrate the benefits of the new technology.

Meet the author

Arpad A. Bergh is president of the Optoelectronics Industry Development Association in Washington; e-mail: [email protected]. This article was excerpted from his May 23, 2005, plenary presentation at the PhAST conference in Baltimore.